Verification of Analytical Methodology for Evaluating GDP Per Capita:

To demonstrate the validity of the analytical methodology

used in the GDP per capita analysis, tsinvestsim(1)

simulations were used to evaluate the convergence of the log-normal

distribution of GDP per capita with population sizes over

five orders of magnitude, (N =

10 to N =

100,000,) and each worker in the workforce

having P = 0.51, f

= rms = 0.02 * 0.5 * 0.41, representing a

maximally optimal efficiency, (P =

0.51, f = rms =

0.02,) with an inefficiency of

0.41 representing the fraction

of the population in the workforce, and each worker in the

workforce operating with an inefficiency of

0.5. These variable values are

representative for the daily values, per worker, of

many industrialized nations.

The output of the tsinvestsim(1)

program was summed into an aggregate GDP using the tsinvestsim-lognormal(1)

program, (source

archive,) to obtain the

mean,

median, and

mode of the simulated GDP, as a

time

series, with a log-normal

distribution, i.e., the GDP per capita distribution.

Since economic data for productivity is available only on a

per capita basis, it is not feasible to determine the

inefficiencies, (they are lumped together.) The

methodology used allows simulations with different variable

values for P, f =

rms, and

avg. For the current

simulations, it is assumed that each worker in the workforce

can operate maximally optimal, P =

0.51, and f = rms =

0.02, (f^2 = rms^2 =

avg, which is maximally optimal, subject to

the Kelly

Criteria,) and f = rms is

decreased to represent the inefficiencies. Note that this

decreases avg by the same

inefficiency factor:

P = ((avg / (k * rms)) + 1) / 2

avg = (k * rms) * ((2 * P) - 1)

Where P is invariant with

k,

(avg is computed by the tsinvestsim(1)

program in this manner) Note, further, that:

rms = sqrt (srms^2 + avg^2)

k * rms = k * sqrt (srms^2 + avg^2)

k * rms = sqrt ((k^2 * srms^2) + (k^2 * avg^2))

k * rms = sqrt ((k * srms)^2 + (k * avg)^2)

indicating that rms can be

multiplied by a constant, k,

without first calculating srms

and avg, then multiplying each

by k, squaring each product, and

finally taking the root-mean-square of the sum of the

squares.

The rationale for selecting variable values in this manner

is that P is a metric on a

worker's ability to synthesize innovation based on new

information, (original, secret, or public,) and

f = rms is a metric on the

wager made on the innovation, with

avg being the return, (positive

or negative,) generated by the innovation, i.e., metrics on

how smart the worker is, and how good a gambler.

If the national GDP per capita, (an aggregate expenditure

approach,) and distribution of income, (an aggregate income

approach,) are analyzed together, the variable values for a

typical worker in the economy can be determined.

In the following simulations, all workers have the same

daily variable values P = 0.51,

and f = rms = 0.02 * 0.5 * 0.41,

(for 51 times out of a hundred innovation success rate, 50%

efficiency at wagering, and 41% of the population in the

workforce,) with each worker starting at I =

$10, (all equal, representing the rural/shared

agricultural economy of the US in 1610,) and the simulations

are all allowed to run for 100,000 days, (about 4 centuries at

250 work days a year,) developing into a log-normal

distribution standard of living, (i.e., GDP growth per

capita,) by 1790, and continuing through 2010. The simulation

outputs are then sampled every 250 days, for annual data, and

all values filtered, prior to 1790, resulting in 1790 through

2010 annual data. The simulation was repeated for workforce

sizes of N = 10, N

= 100, N =

1,000, N =

10,000, and N =

100,000, to verify convergence to the mean of

the simulations.

It should be pointed out, as a concluding remark, that the

objective of the simulations are validity of methodology which

requires only a reasonable approximation to the actual US GDP

per capita-and two digit precision variables is adequate.

Analysis of Simulations:

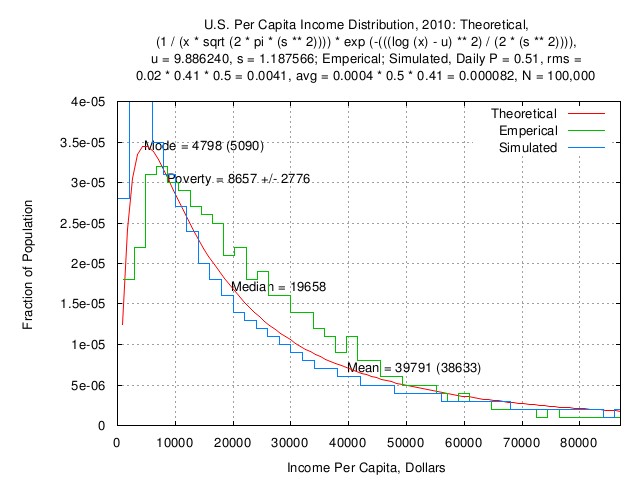

Figure I

Figure I is a plot of the US nominal GDP per capita income

distribution, 2010: theoretical distribution, empirical

distribution, and, simulated distribution (N =

100,000.)

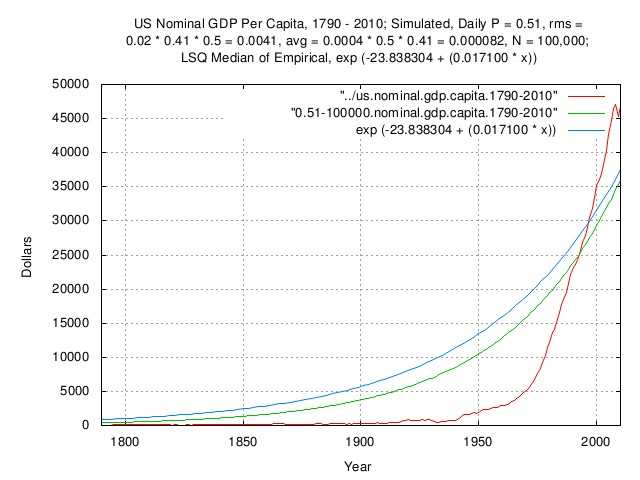

Figure 2

Figure 2 is a plot of the US nominal GDP per capita,

1790-2010: empirical values, simulated values (N

= 100,000,) and Least Squares fit of the

empirical values.

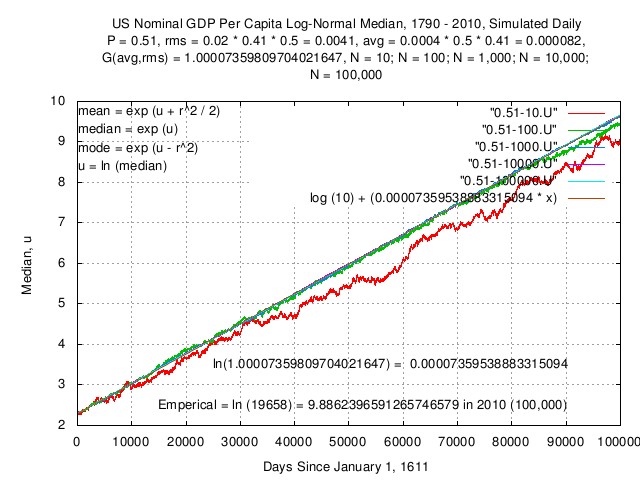

Figure III

Figure III is a plot of the simulated US GDP per capita

log-normal

distribution median, over time, with five orders of magnitude of

population sizes, N, and a plot

of the theoretical values for N =

100,000. Note the convergence to the

theoretical values with increasing

N. Further, note that the values

converged to are independent of

N:

P = 0.51

rms = 0.02 * 0.5 * 0.41

avg = (rms) * ((2 * P) - 1)

= 0.000082

G(avg,rms) = 1.00007359809704021647

Or, the value, V, at a time

x many days, starting with an

initial value of I = 10:

V(x) = I * G(avg,rms)^x

Or:

ln (V(x)) = ln (10) + (x * ln (G(avg,rms)))

= 2.30258509299404568402 + (0.00007359538883315094 * x)

It is important to note that this represents the aggregate

growth in the median of the workforce divided by the size of

the population, (i.e., the median per capita value,) over

time, with the workforce operating at 50% efficiency,

(relative to rms,) and has a

direct mathematical relationship to the typical

worker variable values, rms and

P, on a daily basis. This

function is exponentiated to obtain the median of the log-normal

distribution, over time.

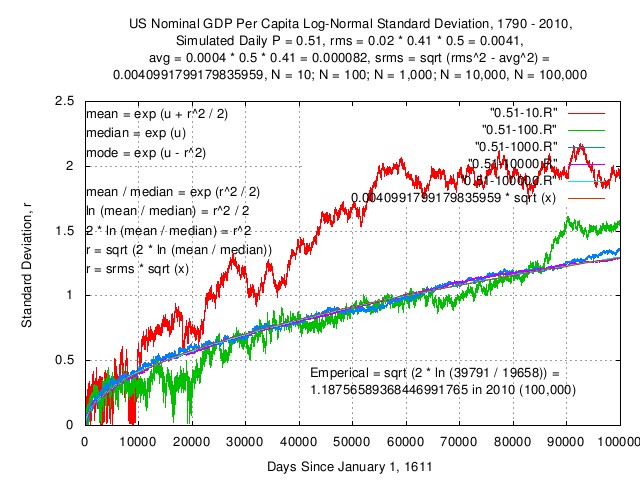

Figure IV

Figure IV is a plot of the simulated US nominal GDP per

capita log-normal

distribution deviation, over time, with five orders of

magnitude of population sizes,

N, and a plot of the theoretical

values for N = 100,000. Note the

convergence to the theoretical values with increasing

N. Further, note that the values

converged to are independent of

N:

P = 0.51

rms = 0.02 * 0.5 * 0.41

avg = (rms) * ((2 * P) - 1)

= 0.000082

srms = sqrt (rms^2 - avg^2)

= 0.0040991799179835959

Or, the value, S, at a time

x many days:

S(x) = srms * sqrt (x)

= 0.0040991799179835959 * sqrt (x)

It is important to note that this represents the standard

deviation of the Gaussian/Normal distribution of the standard

of living of the workforce (i.e., the distribution of the per

capita values,) over time, with the workforce operating at 50%

efficiency, (relative to rms,)

and has a direct mathematical relationship to the

typical worker variable values,

rms and

P, on a daily basis. The square

of this function, divided by two, is exponentiated to obtain

the deviation from the median of the log-normal

distribution, over time.

Further, it is important to note that the

srms of the workers, (or their

typical value of the aggregate,) is related to the

median and mean of the log-normal

distribution at any time.

Analytical Methodology:

Let t be the time interval

the log-normal

distribution has evolved in the data file,

data.file, of the GDP

per capita. Then, in the t'th,

(last,) interval:

u = Mu

r = Rho

median = e^u

mean = e^(u + (r^2 / 2))

mode = e^(u - r^2)

If the data.file

represents GDP per capita data, (i.e., annual GDP divided by

annual population count,) then the file represents

mean GDP per capita

data. One of the issues is to convert the data to

median data.

It is convenient to analyze the evolution of log-normal

distribution, meaning by time,

t:

median(t) = e^u(t)

mean(t) = e^(u(t) + (r(t)^2 / 2))

mode(t) = e^(u(t) - r(t)^2)

where for economic data, (like the US GDP per capita,) the

mean(t) historical time

series and the median(t),

mean(t), and

mode(t) are available only at

one point in time, (usually the last interval.)

mean(t) = e^(u(t) + (r(t)^2 / 2))

mode(t) = e^(u(t) - r(t)^2)

mean(t) = e^(u(t)) * e^(r(t)^2 / 2)

mode(t) = e^(u(t)) / e^(r(t)^2)

mean(t) / mode(t) = (e^(u(t)) * e^(r(t)^2 / 2)) / (e^(u(t)) / e^(r(t)^2))

mean(t) / mode(t) = (e^(r(t)^2 / 2)) / (1 / e^(r(t)^2))

mean(t) / mode(t) = (e^(r(t)^2 / 2)) * e^(r(t)^2)

mean(t) / mode(t) = e^((r(t)^2 / 2) + r(t)^2)

mean(t) / mode(t) = e^(r(t)^2 * (1 + (1 / 2)))

mean(t) / mode(t) = e^((3 / 2) * r(t)^2)

ln (mean(t) / mode(t)) = (3 / 2) * r(t)^2

r(t)^2 = (2 / 3) * ln (mean(t) / mode(t))

r(t) = sqrt ((2 / 3) * ln (mean(t) / mode(t)))

r(t) = srms * sqrt (t)

r(t)^2 = srms^2 * t

mean(t) = e^(u(t) + (r(t)^2 / 2))

u(t) = a + (b * t)

mean(t) = e^(a + (b * t) + (srms^2 * t / 2))

mean(t) = e^(a + (b * t) + ((srms^2 / 2) * t))

mean(t) = e^(a + ((b + (srms^2 / 2)) * t))

median(t) = e^u(t) = e^(a + (b * t))

with a and

b determined by LSQ of

mean(t).

Validation:

Unfortunately, the tsinvestsim-lognormal(1)

program does not provide the

mode(t) but as an alternative

derivation using the median(t)

and mean(t) for analysis of the

simulation:

mean(t) = e^(u(t) + (r(t)^2 / 2))

mean(t) = e^u(t) * e^(r(t)^2 / 2)

median(t) = e^u(t)

mean(t) = e^u(t) * e^(r(t)^2 / 2)

mean(t) / median(t) = e^u(t) * e^(r(t)^2 / 2) / e^u(t)

mean(t) / median(t) = e^(r(t)^2 / 2)

r(t)^2 / 2 = ln (mean(t) / median(t))

r(t)^2 = 2 * ln (mean(t) / median(t))

r(t) = sqrt (2 * ln (mean(t) / median(t)))

r(t) = srms * sqrt (t)

srms = r(t) / sqrt (t)

mean(t) = e^(a + ((b + (srms^2 / 2)) * t))

ln (mean(t)) = a + ((b + (srms^2 / 2)) * t)

The actual values used in the simulation:

P = 0.51, f = 0.02 * 0.50 * 0.41 = 0.0041

f = rms = 0.02 * 0.50 * 0.41 = 0.0041

0.51 = ((avg / 0.0041) + 1) / 2

avg = 0.0041 * ((2 * 0.51) - 1)

= 0.000082

srms = sqrt (rms^2 - avg^2)

= sqrt (0.0041^2 - 0.000082^2)

= 0.0040991799179835959

G(avg,rms) = G(0.0041 * ((2 * 0.51) - 1),0.02 * 0.50 * 0.41)

= 1.00007359809704021647

G(t) = 10 * (1.00007359809704021647^t)

ln (G(t)) = ln (10) + (t * ln (1.00007359809704021647))

= 2.30258509299404568402 + (0.00007359538883315094 * t)

ln (mean(t)) = a + ((b + (srms^2 / 2)) * t)

a = 2.30258509299404568402

b + (srms^2 / 2) = 0.00007359538883315094

b = 0.00007359538883315094 - (srms^2 / 2)

= 0.00007359538883315094 - (0.0040991799179835959^2 / 2)

= 0.00006519375083315094

ln(mean(t)) = 2.30258509299404568402 + (0.00007359538883315094 * t)

And, analyzing the data from the simulations, (the order of

the fields from tsinvestsim-lognormal(1)

program): "time,

minimum,

median,

mean,

maximum",):

cut -f4 0.51-10 | tslsq -e -p

e^(2.243692 + 0.000091t)

cut -f4 0.51-10 | tsfraction | tsavg -p

0.000089

cut -f4 0.51-10 | tsfraction | tsrms -p

0.002662

G(0.000089,0.002662) = 1.00008546072723226738

ln (G(0.000089,0.002662)) = 0.00008545707567235967

egrep '^99999' 0.51-10

99999 1906.627099 8477.783394 52569.322616 387424.213469

r(100000) = sqrt (2 * ln (52569.322616 / 8477.783394))

= 1.91033175441258050009

srms = 1.91033175441258050009 / sqrt (100000)

= 0.00604099943048917012

r(t) = srms * sqrt (t)

r(t) = 0.00604099943048917012 * sqrt (t)

r(t)^2 / 2 = 0.00001824683705958524 * t

ln (mean(t)) = a + ((b + (srms^2 / 2)) * t)

a = 2.243692

b = 0.000091 - (0.00604099943048917012^2 / 2)

= 0.00007275316294041476

u(t) = 2.243692 + (0.00007275316294041476 * t)

cut -f4 0.51-100 | tslsq -e -p

e^(2.230331 + 0.000083t)

cut -f4 0.51-100 | tsfraction | tsavg -p

0.000084

cut -f4 0.51-100 | tsfraction | tsrms -p

0.000736

G(0.000084,0.000736) = 1.00008373267247867903

ln (G(0.000084,0.000736)) = 0.00008372916709413426

egrep '^99999' 0.51-100

99999 290.545725 12589.060312 43569.000789 1248187.418192

r(100000) = sqrt (2 * ln (43569.000789 / 12589.060312))

= 1.57576501978003208644

srms = 1.57576501978003208644 / sqrt (100000)

= 0.00498300651972517984

r(t) = srms * sqrt (t)

r(t) = 0.00498300651972517984 * sqrt (t)

r(t)^2 / 2 = 0.00001241517698781182 * t

ln (mean(t)) = a + ((b + (srms^2 / 2)) * t)

a = 2.230331

b = 0.000083 - (0.00498300651972517984^2 / 2)

= 0.00007058482301218818

u(t) = 2.230331 + (0.00007058482301218818 * t)

cut -f4 0.51-1000 | tslsq -e -p

e^(2.289082 + 0.000082t)

cut -f4 0.51-1000 | tsfraction | tsavg -p

0.000083

cut -f4 0.51-1000 | tsfraction | tsrms -p

0.000220

G(0.000083,0.000220) = 1.00008297924392550143

ln (G(0.000083,0.000220)) = 0.00008297580133848107

egrep '^99999' 0.51-1000

99999 101.798190 15302.138722 38246.692966 987378.496244

r(100000) = sqrt (2 * ln (38246.692966 / 15302.138722))

= 1.35356159353659762681

srms = 1.35356159353659762681 / sqrt (100000)

= 0.00428033758890269486

r(t) = srms * sqrt (t)

r(t) = 0.00428033758890269486 * sqrt (t)

r(t)^2 / 2 = 0.00000916064493748667 * t

ln (mean(t)) = a + ((b + (srms^2 / 2)) * t)

a = 2.289082

b = 0.000082 - (0.00428033758890269486^2 / 2)

= 0.00007283935506251333

u(t) = 2.289082 + (0.00007283935506251333 * t)

cut -f4 0.51-10000 | tslsq -e -p

e^(2.299558 + 0.000082t)

cut -f4 0.51-10000 | tsfraction | tsavg -p

0.000082

cut -f4 0.51-10000 | tsfraction | tsrms -p

0.000105

G(0.000082,0.000105) = 1.00008199784944121253

ln (G(0.000082,0.000105)) = 0.00008199448780131961

egrep '^99999' 0.51-10000

99999 173.857625 15894.484298 36704.069587 1771254.349566

r(100000) = sqrt (2 * ln (36704.069587 / 15894.484298))

= 1.29376619780877467417

srms = 1.29376619780877467417 / sqrt (100000)

= 0.00409124794481167259

r(t) = srms * sqrt (t)

r(t) = 0.00409124794481167259 * sqrt (t)

r(t)^2 / 2 = 0.00000836915487296287 * t

ln (mean(t)) = a + ((b + (srms^2 / 2)) * t)

a = 2.299558

b = 0.000082 - (0.00409124794481167259^2 / 2)

= 0.00007363084512703713

u(t) = 2.299558 + (0.00007363084512703713 * t)

cut -f4 0.51-100000 | tslsq -e -p

e^(2.300291 + 0.000082t)

cut -f4 0.51-100000 | tsfraction | tsavg -p

0.000082

cut -f4 0.51-100000 | tsfraction | tsrms -p

0.000085

G(0.000082,0.000085) = 1.00008199974949315241

ln(G(0.000082,0.000085)) = 0.00008199638769747028

egrep '^99999' 0.51-100000

99999 39.190364 15804.790282 36694.603142 11503692.146641

r(100000) = sqrt (2 * ln (36694.603142 / 15804.790282))

= 1.29793421590474711612

srms = 1.29793421590474711612 / sqrt (100000)

= 0.00410442837532374379

r(t) = srms * sqrt (t)

r(t) = 0.00410442837532374379 * sqrt (t)

r(t)^2 / 2 = 0.00000842316614408135 * t

ln (mean(t)) = a + ((b + (srms^2 / 2)) * t)

a = 2.300291

b = 0.000082 - (0.00410442837532374379^2 / 2)

= 0.00007357683385591865

u(t) = 2.300291 + (0.00007357683385591865 * t)

Note that:

tsfraction data.file | tsrms -p

rms

is meaningless, (as far as productivity per capita is

concerned,) since the natural evolution of the log-normal

distribution of the aggregate GDP per capita, will be,

given enough time and population, a near perfect exponential

where avg = rms, and

P = 1. The

rms of the workers, (or per

capita value of the aggregate,) must be determined from the

mean(t),

mode(t), and the

median(t) of the distribution at

some time interval, t, (usually

the last interval.)

Empirical GDP per capita data can present situations where

the long term avg and

rms are not nearly equal, which

is usually due to governance issues that effect all, (or

most,) of the workforce, and rms

is greater than

avg. Subtracting, (via

root-mean-square,) the typical individual

rms from the GDP per capita

rms offers a methodology for

analysis of the governance issues, providing the log-normal

distribution has evolved for a sufficient time, and the

population size is sufficiently large.

Simulation:

As a concluding note, to align the simulations,

(mean-variance simulations of geometric Brownian motion

fractals are notoriously unstable,) with the empirical data, 4

data points had to align with the empirical data: the mean of

the simulated nominal US GDP per capita with the empirical

nominal US GDP per capita at 1790; the simulated nominal US

GDP per capita with the empirical nominal US GDP per capita at

2010; and the median; and mean of the log-normal

distribution of the productivity/income of the simulated

nominal US GDP per capita with the empirical nominal US GDP

per capita at 2010. There are 3 variables, which interact:

I, the starting value for each

worker, (I = $10, in 1610, which

was used as a scaling factor);

avg; and,

rms. Lowering both

avg and

rms will decrease the ratio of

the mean to the median in 2010, and, increasing

avg, relative to

rms, will increase the growth in

the nominal US GDP per capita in the simulation. The number of

workers, N, contributing to the

simulated nominal US GDP per capita was increased, in steps of

orders of magnitude, until the simulations converged to their

mean, indicating sufficient accuracy for comparison with the

empirical data. Note that the log-normal

distribution income empirical data for 2010 is in 2010

nominal dollars, necessitating an analysis of nominal US GDP

per capita, (as opposed to the traditional real GDP per

capita.) The empirical log-normal

distribution income in 1790 is not available or known,

necessitating starting the simulation about two centuries

before any data of interest to the analysis to allow a log-normal

distribution income to evolve by 1790. The tsinvestsim(1)

program from the NtropiX

site, (in the tsinvest

archive,) was used to generate the individual worker and

nominal US GDP per capita time

series for the simulation. The simulation for

N = 100,000 took about 20 hours

on a 2.5GHz machine.

calc(1) Macros:

The following calc(1)

macros were used for calculation of

P(avg,rms) and

G(avg,rms) in ~/.calcrc:

define P (avg, rms) = ((avg / rms) + 1) / 2;

define G (avg, rms) = power (1 + rms, ((avg / rms) + 1) / 2) * \

power (1 - rms, 1 - ((avg / rms) + 1) / 2);

The following calc(1)

script is for computing avg,

rms, and,

G(avg,rms), given

srms and

G obtained empirically from a time

series.

#!/usr/local/bin/calc -d -f

#

# A license is hereby granted to reproduce this design for personal,

# non-commercial use.

#

# THIS DESIGN IS PROVIDED "AS IS". THE AUTHOR PROVIDES NO WARRANTIES

# WHATSOEVER, EXPRESSED OR IMPLIED, INCLUDING WARRANTIES OF

# MERCHANTABILITY, TITLE, OR FITNESS FOR ANY PARTICULAR PURPOSE. THE

# AUTHOR DOES NOT WARRANT THAT USE OF THIS DESIGN DOES NOT INFRINGE

# THE INTELLECTUAL PROPERTY RIGHTS OF ANY THIRD PARTY IN ANY COUNTRY.

#

# So there.

#

# Copyright (c) 1992-2015, John Conover, All Rights Reserved.

#

# Comments and/or problem reports should be addressed to:

#

# john@email.johncon.com

#

# http://www.johncon.com/john/

# http://www.johncon.com/ntropix/

# http://www.johncon.com/ndustrix/

# http://www.johncon.com/nformatix/

# http://www.johncon.com/ndex/

#

# A calc(1) script for binary search-for-solution of: given, srms and

# g; find avg, rms, and, G(avg,rms).

#

# Both the domain and range, between "top" and "bottom" must be

# monotonic increasing on avg; G(avg,rms) is monotonic increasing on

# increasing avg, (starting with avg = rms = 1 to avoid division by

# zero in the calculation of the first iteration of G(avg,rms), and

# start the binary search at avg = 0.5.)

#

# The variables srms and g, are required. The variable g is G(avg,rms)

# to search for, (and must be greater than unity,) given srms, (which

# must be greater than zero):

#

# Real US GDP:

#

srms = 0.02126296324279258349;

g = 1.0170171123188325426;

#

# Nominal US GDP:

#

# srms = 0.02126296324302608945;

# g = 1.02982917935065044642;

#

top = 1;

bottom = 0;

avg = 1;

rms = 1;

temp = 0.0;

#

while (abs ((temp = G(avg,rms)) - g) > 0.0000000000000000001)

{

if (temp < g)

{

bottom = bottom + ((top - bottom) / 2.0);

avg = bottom + ((top - bottom) / 2.0);

rms = sqrt (avg^2 + srms^2);

/* printf ("1: avg = %f, rms = %f, G(avg,rms) = %f\n", avg, rms, temp); */

}

else

{

top = top - ((top - bottom) / 2.0);

avg = top - ((top - bottom) / 2.0);

rms = sqrt (avg^2 + srms^2);

/* printf ("2: avg = %f, rms = %f, G(avg,rms) = %f\n", avg, rms, temp); */

}

}

#

printf ("avg = %f, rms = %f, G(avg,rms) = %f\n", avg, rms, temp);

License

The information contained herein is private and

confidential and dissemination is strictly forbidden, except

under the provisions of contractual license.

THE AUTHOR PROVIDES NO WARRANTIES WHATSOEVER, EXPRESSED OR

IMPLIED, INCLUDING WARRANTIES OF MERCHANTABILITY, TITLE, OR

FITNESS FOR ANY PARTICULAR PURPOSE. THE AUTHOR DOES NOT

WARRANT THAT USE OF THIS INFORMATION DOES NOT INFRINGE THE

INTELLECTUAL PROPERTY RIGHTS OF ANY THIRD PARTY IN ANY

COUNTRY.

So there.

Copyright © 1992-2015, John Conover, All Rights

Reserved.

Comments, questions, and problem reports should be

addressed to:

- john@email.johncon.com

- http://www.johncon.com/john/

- http://www.johncon.com/ntropix/

- http://www.johncon.com/ndustrix/

- http://www.johncon.com/nformatix/

- http://www.johncon.com/ndex/

|